London-based investment manager Triple Point Group is set to test DIY investor appetite for private credit exposure this week, as it prepares to launch a high-yielding bond under its Secured Fixed Income plc (SFI) subsidiary.

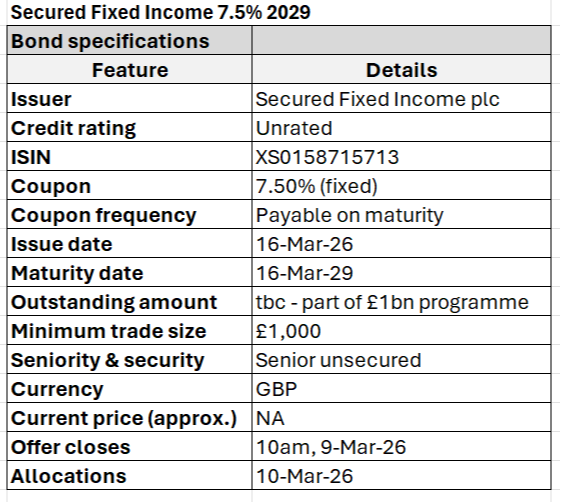

The retail-accessible Secured Fixed Income 7.5% 16/03/29 bond, for which applications close on Monday 9 March, has been structured with a yield-hungry audience in mind: there’s an eye-catching 7.5 per cent coupon on offer, and its short-term maturity should limit price volatility.

However, as with much in life, there is seldom such a thing as a free lunch. While the imminent bond offers an enticing coupon at first glance, it is worth considering what strings might come attached. We set out some quick analysis on the pending new issue below.

The first question any investor should ask when faced with such a material yield uplift over investment grade corporate bonds is, who am I gaining exposure to?

The bond marks the debut issuance under a newly established £1bn bond programme from SFI, a private entity which lends to primarily UK-based small enterprises. The group engages in both straightforward business lending, as well as riskier instruments such as mezzanine debt. It also invests in real estate, infrastructure and venture capital, taking on potentially more illiquid positions through special purpose vehicles. To be clear: this is private-credit-style exposure, which carries an elevated level of risk from the off.

What to be aware of

While the bond prospectus defines the offer as ‘secured’, which is typically considered safer debt and well-suited for retail investors, the caveat is that the security is against an underlying book of private loans – an asset class that tends to be less liquid and is often tricky to value. This does not automatically signal a higher risk investment, but keep in mind that recovering capital in a downturn would rely heavily on the quality of SFI’s small enterprise loan book.

In addition, the issuer is privately owned and unrated by credit agencies. This means investors must rely upon their own assessment of SFI’s latest financials to gauge the default risk.

More detailed information about the metrics you can use to understand a company’s financial health can be found in my last column, but from a quick review of the accounts, SFI’s financial leverage is not insignificant, and it maintains a slim equity buffer. Net assets of £5.6mn stand against non-current liabilities of £50.5mn as at 30 September 2025.

Most tellingly, SFI’s interest cover ratio came in at 2.1 for the half year – a slight improvement on multiples of 1.8 in both FY25 and FY24. This metric indicates how comfortably a company can cover its interest payments, with ratios below two considered fairly risky.

This perhaps explains the choice of coupon payment schedule. SFI is offering a fixed coupon that is compounded annually and paid in full at maturity, rather than a more conventional periodic payment structure, in which interest is paid in regular intervals over the life of the bond.

Bankers refer to this as a rolled-up structure, and it introduces an element of increased credit risk: a lack of regular interest payments deprives investors of an early warning system for default risk.

This means bondholders will receive no cash flow until maturity, and should SFI default, investors risk losing both the face value of the bond plus the compounded interest. Investing in this kind of structure requires careful consideration indeed.

The Investors’ Chronicle view

While the rolled-up structure could appeal to those seeking a lump sum on a short time horizon, it may deter investors focused on capital preservation, or seeking a steadier stream of interim income over a longer time frame. In any case, it would likely best serve an already diversified portfolio in a small allocation.

Investors can apply for allocations through stockbrokers and investment platforms including Hargreaves Lansdown, Interactive Investor, and AJ Bell.

Ultimately, this security is a much riskier investment than a corporate bond from a rated and listed entity such as Vodafone (VOD) or Tesco (TSCO), and the coupon on offer reflects this.

The premium you get should be weighed carefully against the elevated credit risk and structural complexity that you would be taking on: a speculative investment where a full return is dependent on the performance of SFI’s portfolio of private loans.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment