For nearly three years, the artificial intelligence (AI) narrative revolved around one critical piece of hardware: the graphics processing unit (GPU). Now, as hyperscalers accelerate their data center build-outs, investors are realizing that GPUs are only one layer in the AI chip stack.

Memory chips and other data storage devices are integral complements to GPU clusters, and demand for them has surged. As a result, over the last year, shares of flash memory specialist Sandisk (SNDK 5.69%) have skyrocketed by over 1,600%.

Yet based on the tailwinds fueling Sandisk’s business, I think the stock’s rally could just be getting started. In my view, it could easily deliver further multibagger returns from here.

Today’s Change

(-5.69%) $-37.30

Current Price

$618.13

Key Data Points

Market Cap

$91B

Day’s Range

$612.23 – $651.55

52wk Range

$27.89 – $725.00

Volume

5.7K

Avg Vol

17M

Gross Margin

34.81%

Why is memory important for AI models?

Throughout the AI revolution, growth investors have primarily been focused on two aspects of the AI market: GPU designers such as Nvidia and Advanced Micro Devices, and cloud infrastructure providers like Microsoft, Amazon, and Alphabet.

Businesses that provide memory and data storage were largely underappreciated because those products were seen as commoditized. Rival offerings lacked much differentiation, and their sales outlooks often relied on the upgrade cycles in the consumer electronics market. That narrative has begun to shift, however.

High-performance computing is not supported by processing power alone. As AI models scale up, big tech companies must make additional investments in their data centers’ ability to handle inference workloads — in other words, the processing tasks involved in using trained models to make predictions and decisions based on real-world data.

These workloads are incredibly memory-intensive, as they require large volumes of data to be rapidly accessible. As such, Sandisk’s high-speed NAND flash storage chips are becoming essential for AI servers.

Image source: Getty Images.

What is Sandisk’s addressable market?

The NAND flash memory market is expected to grow from roughly $59 billion in 2026 to $76 billion by 2031 — a 5.3% compound annual growth rate. On the surface, this growth rate may not appear exciting. However, consider that during Sandisk’s fiscal 2026 second quarter (which ended Jan. 2), 85% of the company’s revenue stemmed from its consumer electronics segment and its edge segment (which makes memory for devices like PCs and smartphones). The subtle winner in the company’s latest earnings report was its data center division — which grew faster than its other business lines at 64% quarter over quarter.

But with only $440 million in quarterly data center sales — compared to $2.6 billion for its edge and consumer electronics segments combined — Sandisk is clearly still in the early stages of penetrating the AI data center market. Its data center opportunity is positioned for explosive growth as demand for NAND flash storage accelerates.

Moreover, given limited competitive dynamics in the memory space — Micron, SK Hynix, and Samsung are the other core players — Sandisk should be able to command some level of pricing power as it continues to attract enterprise and hyperscaler customers.

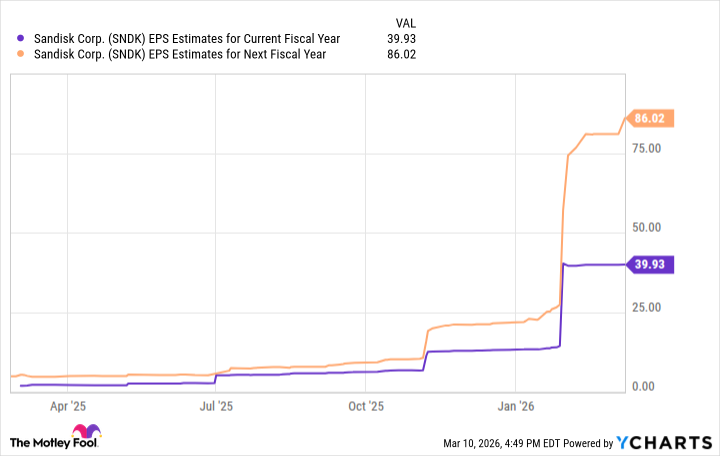

SNDK EPS Estimates for Current Fiscal Year data by YCharts.

Wall Street appears bullish on Sandisk’s ability to maintain strong profit margins. The analysts’ consensus is that earnings will double over the next two years as the company rides the secular tailwinds of the AI supercycle.

How much higher can Sandisk stock go?

While Sandisk stock has been on a monster run, looking at its percentage gains in isolation doesn’t tell us too much about the company’s underlying valuation profile. Currently, it is trading at a forward price-to-earnings (P/E) multiple of 15.5.

This is heavily discounted compared to other category-defining AI chip stocks. Nvidia, AMD, and Broadcom have witnessed forward P/E ratios well above 40 during prior bull cycles in the AI revolution.

With that said, measuring Sandisk against those companies is a bit of an apples-to-oranges comparison. GPU and AI accelerator designers are more versatile, general-purpose players in generative AI development. Sandisk’s expertise in flash storage — while critical — is more niche. Hence, the company’s addressable market isn’t as large.

I think a more appropriate comparison for Sandisk is to the tech-heavy Nasdaq-100 index, which has a forward P/E of about 24. If the market boosts Sandisk’s valuation so that it trades in line with the index, it could be knocking on a price of nearly $1,000 per share by year’s end. This would amount to a gain of more than 50% from the current price.

Considering Wall Street steeply underestimated hyperscalers’ planned capital expenditures for 2026, I think Sandisk is strategically positioned for higher-than-expected growth this year. The stock’s upside could be much higher than 50%.

With the company’s data center business ready for liftoff and its enormous opportunity in NAND flash storage, Sandisk stock could feasibly double in 2026 should the company exceed Wall Street’s expectations — which I think is highly probable.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment