Artificial intelligence (AI) computing power has mostly been allocated to training large language models (LLMs) so far, but a shift is now happening in this space. Inference, which is the process of putting trained AI models to work in real-world situations by exposing them to new data and queries, is expected to account for the majority of AI computing power.

According to McKinsey, inference will account for more than half of AI computing capacity in data centers by 2030, surpassing the training phase. This explains why demand for central processing units (CPUs) is now increasing at a robust pace, as they are considered ideal for handling AI inference workloads due to lower costs.

In fact, Advanced Micro Devices (AMD +7.23%) doubled its server CPU total addressable market (TAM) estimate last month to $120 billion by 2030, noting that demand for these chips is increasing due to agentic AI and inference applications. AMD, however, isn’t the only one benefiting from the improving CPU demand.

Intel (INTC +2.86%) is the dominant player in the server CPU market, suggesting it may be better positioned to capitalize on this massive opportunity. However, there is more than what meets the eye in this space, which is why we will take a closer look at AMD and Intel’s positioning in server CPUs to find out which of these two semiconductor stocks is a better play on the growing inference demand.

Image source: The Motley Fool.

Intel dominates server CPUs, but AMD is quickly closing the gap

According to Mercury Research, Intel accounted for almost 67% of the server CPU market at the end of the first quarter of 2026. AMD accounted for the rest of the market. However, what’s worth noting is that Intel has been consistently losing ground to AMD.

Today’s Change

(2.86%) $3.56

Current Price

$128.13

Key Data Points

Market Cap

$626B

Day’s Range

$126.67 – $132.58

52wk Range

$18.96 – $132.75

Volume

3.5M

Avg Vol

128.3M

Gross Margin

35.90%

Intel was way more dominant in server CPUs four years ago, controlling just over 88% of the market in the first quarter of 2022. AMD has significantly dented Intel’s position in server CPUs by offering better products, enabling it to attract more customers. What’s more, AMD is enjoying stronger pricing power in this space despite holding a significantly lower unit share.

This is evident from the fact that AMD’s revenue share of server CPUs stood at a record 46.2% in Q1, suggesting that the average selling price (ASP) of its products is higher. Customers have been willing to pay more for AMD’s server processors because of their performance and cost advantages. The good news for AMD investors is that it expects to corner a bigger share of the server CPU market in 2026.

AMD anticipates a 70% jump in server CPU revenue in the second quarter of 2026. Additionally, management sees the “robust growth continuing through the second half of 2026 and into 2027 as we ramp our next-generation EPYC processors.”

Intel, meanwhile, is hamstrung by a short supply of its server CPUs. Intel management noted on the April earnings call that “demand continues to run ahead of supply for all our businesses, especially for Xeon server CPUs” despite the company’s efforts to improve factory output. However, the good news for Intel stock investors is that the company is “seeing strong and sustained momentum” for Xeon server CPUs.

Intel also points out that the ratio of server CPU deployment in data center accelerators, compared to graphics processing units (GPUs), is now favoring CPUs. Moreover, Intel may be able to arrest the market-share slide thanks to its partnership with Nvidia, which has decided to use the Xeon 6 processor in its Vera Rubin server racks.

Also, Intel is looking to prevent AMD from gaining more share by ramping up the production of its server CPUs based on the 18A architecture, which it claims could deliver a 30% performance gain and a 50% efficiency lead over AMD’s Epyc processors. Intel, however, will need to ensure that it can produce enough of these chips to stop AMD from making further gains in server CPUs.

The valuation makes it easier to decide which one is the better buy now

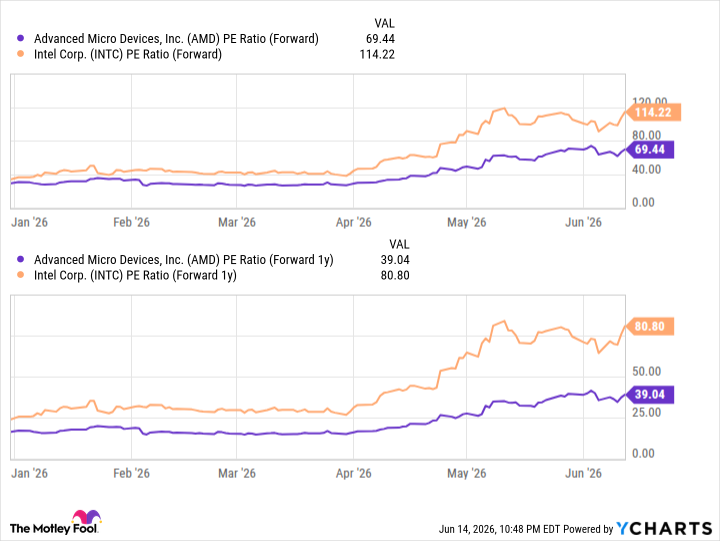

Both Intel and AMD have seen a significant spike in their stock prices this year. Intel is up 216%, as of this writing, while AMD stock has gained 129%. This explains why AMD is significantly cheaper than Intel.

Data by YCharts

Also, consensus estimates suggest that AMD’s earnings growth will significantly outpace Intel’s. Specifically, AMD’s bottom line is expected to jump by nearly 78% in 2027, well above the 42% jump predicted for Intel. Also, AMD’s growing influence in the data center GPU market, where it has lucrative contracts with major hyperscalers and AI companies, is another reason why it is the better pick over Intel.

After all, Intel has been finding it tough to crack the data center GPU market, giving AMD a distinct advantage in AI chips. In the end, it can be concluded that AMD’s relatively cheaper valuation, stronger earnings growth, and opportunities in the GPU market make it a better AI stock to capitalize on the growing inference demand.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment