C3.ai (AI +4.97%) was one of the world’s first enterprise artificial intelligence (AI) companies. Today, it offers over 40 ready-made applications that help businesses deploy this revolutionary technology in a fast and cost-effective manner. However, the company’s long-term shareholders have been on a wild ride which has, unfortunately, culminated in steep losses since its initial public offering (IPO).

The company went public in December 2020 at $42 per share, before quickly soaring to an all-time high of $161 during that same month. However, it has trended lower ever since, and despite some attempted recoveries along the way, it is now trading at an all-time low of around $8. It’s sitting on a year-to-date loss of 36% in 2026 alone, as the company’s new CEO struggles to stabilize its financial results following the departure of its founder, Thomas Siebel, last September due to health issues.

But the emerging AI industry continues to boom. Could this be the ultimate chance to buy C3.ai stock at a heavy discount to its all-time high, or should investors steer clear?

Image source: Getty Images.

A unique business model

Developing AI software from scratch requires significant financial and technical resources, which the average business simply doesn’t have. C3.ai’s portfolio of ready-made applications is an affordable pathway to AI adoption, especially because they can be customized to suit very specific requirements.

These apps are crafted for a variety of different industries. For financial institutions, the C3.ai Anti-Money Laundering app helps identify suspicious transactions with a much higher degree of accuracy than traditional methods, and it gets better over time as it absorbs more real-world data. For manufacturers, the C3.ai Inventory Optimization app is an advanced forecasting tool that has reduced inventory holding costs by up to 52% for some clients.

Those are just a couple of examples. Another benefit that C3.ai provides is accessibility — businesses can access and deploy its apps through major cloud platforms like Amazon Web Services, Microsoft Azure, and Alphabet‘s Google Cloud. They can tap into the computing capacity on offer from their chosen cloud provider to rapidly scale their C3.ai apps as necessary, so they can grow seamlessly without constraints.

Revenue is shrinking at a rapid pace

C3.ai generated $53.3 million in total revenue during its fiscal 2026 third quarter (ended Jan. 31), which was a whopping 46% decline from the year-ago period. It was also substantially below management’s forecasted range of $72 million to $80 million. That’s a big reason why the company’s stock plummeted by more than 20% in after-hours trading following the release of these results.

The weak top line caused C3.ai’s generally accepted accounting principles (GAAP) net loss to balloon by 66% to $133.4 million during the quarter. This was bad news, since the company now only has $621.9 million in cash, equivalents, and marketable securities remaining on its balance sheet. In other words, management has to find more revenue very quickly, or it will have to slash costs dramatically.

Today’s Change

(4.97%) $0.43

Current Price

$9.08

Key Data Points

Market Cap

$1.2B

Day’s Range

$8.41 – $9.20

52wk Range

$7.72 – $30.24

Volume

143K

Avg Vol

7.1M

Gross Margin

46.77%

Reducing expenses was the primary focus of C3.ai’s new CEO, Stephen Ehikian, during the third quarter. This should narrow the company’s losses in the future. The adjustments involved flattening the sales department to make it more efficient, which could solve some of the issues that appeared after Thomas Siebel departed last September.

Siebel played a pivotal role in closing many of C3.ai’s largest deals and maintaining some of its most important client relationships, and he heavily underestimated the effect of his decision to step away. Unfortunately, this is common in founder-led companies — if Elon Musk left Tesla, or Mark Zuckerberg left Meta Platforms, their companies would almost certainly lose some of their flair.

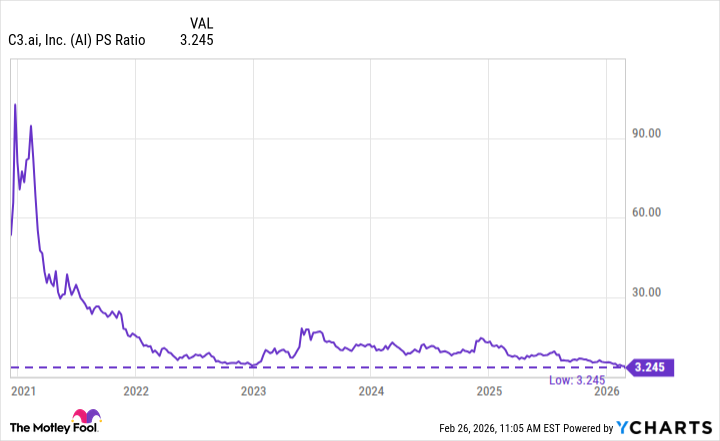

C3.ai stock is trading at a record low valuation

C3.ai stock was trading at a sky-high price-to-sales (P/S) ratio of over 90 when its stock peaked in 2020, which was completely unsustainable. But the stock’s continued plunge has pushed its P/S ratio down to just 3.2, which is its cheapest level since it went public.

AI PS Ratio data by YCharts.

However, a beaten-down stock isn’t always a cheap stock. Investors typically don’t like buying into shrinking businesses because of their potential to destroy value over time, and C3.ai currently expects its fiscal 2026 fourth-quarter revenue to come in even lower than its third-quarter revenue. With no growth in sight, it’s very difficult to make a case for buying this stock right now.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment