![]()

Add Silicon Canals to your Google News feed. ![]()

Japan’s robotics industry recorded its highest quarterly order volume in history during the first three months of 2025, as manufacturers across Asia, North America, and Europe scramble to fill gaps left by aging workforces and persistent labor shortages.

The Japan Robot Association (JARA) reported that orders for industrial robots reached ¥324.5 billion ($2.2 billion) in Q1 2025, a 14.2% increase year-over-year and the strongest quarter since the association began tracking data in the 1980s. Export orders, which account for roughly 70% of total shipments, drove much of the growth, with demand surging from China, South Korea, the United States, and Germany.

The demographics behind the machines

People in their 50s and 60s across Japan’s manufacturing heartland know exactly what these numbers mean. They’ve watched their factory floors thin out, year by year, as younger workers moved to cities or chose service-sector careers over industrial ones. Japan’s working-age population has contracted by over 10 million since its peak in the mid-1990s, and the country now has 1.24 job openings for every applicant, according to the Ministry of Internal Affairs and Communications.

But this is far from a uniquely Japanese problem. South Korea’s fertility rate fell to 0.72 in 2024, the lowest of any major economy. Germany’s industrial workforce is projected to shrink by 7 million workers by 2035. Even countries with younger populations, like Vietnam and Indonesia, are seeing manufacturing labor costs rise fast enough that automation has become economically attractive for the first time.

The result: a global market for industrial robots projected to reach $35.2 billion by 2028, according to MarketsandMarkets, up from $20.3 billion in 2023.

China is the biggest buyer, and the biggest competitor

China remains the world’s largest consumer of industrial robots, absorbing more than half of global shipments in 2024. Chinese factories installed approximately 290,000 units last year, driven by the government’s “Made in China 2025” strategy and an accelerating push to offset its own demographic decline. China’s working-age population peaked in 2011 and has been contracting since.

Yet China is also rapidly becoming Japan’s most formidable rival in the robotics space. Companies like FANUC and Yaskawa Electric, long dominant in the global market, now face growing competition from Chinese manufacturers such as Estun Automation and SIASUN, which offer comparable products at significantly lower price points. A study by the International Federation of Robotics found that Chinese-made robots accounted for 29% of domestic installations in 2024, up from just 15% five years earlier.

For Japan’s robotics giants, the record order numbers carry an undertone of urgency. They know the window of technological superiority is narrowing.

The new wave: collaborative robots and AI integration

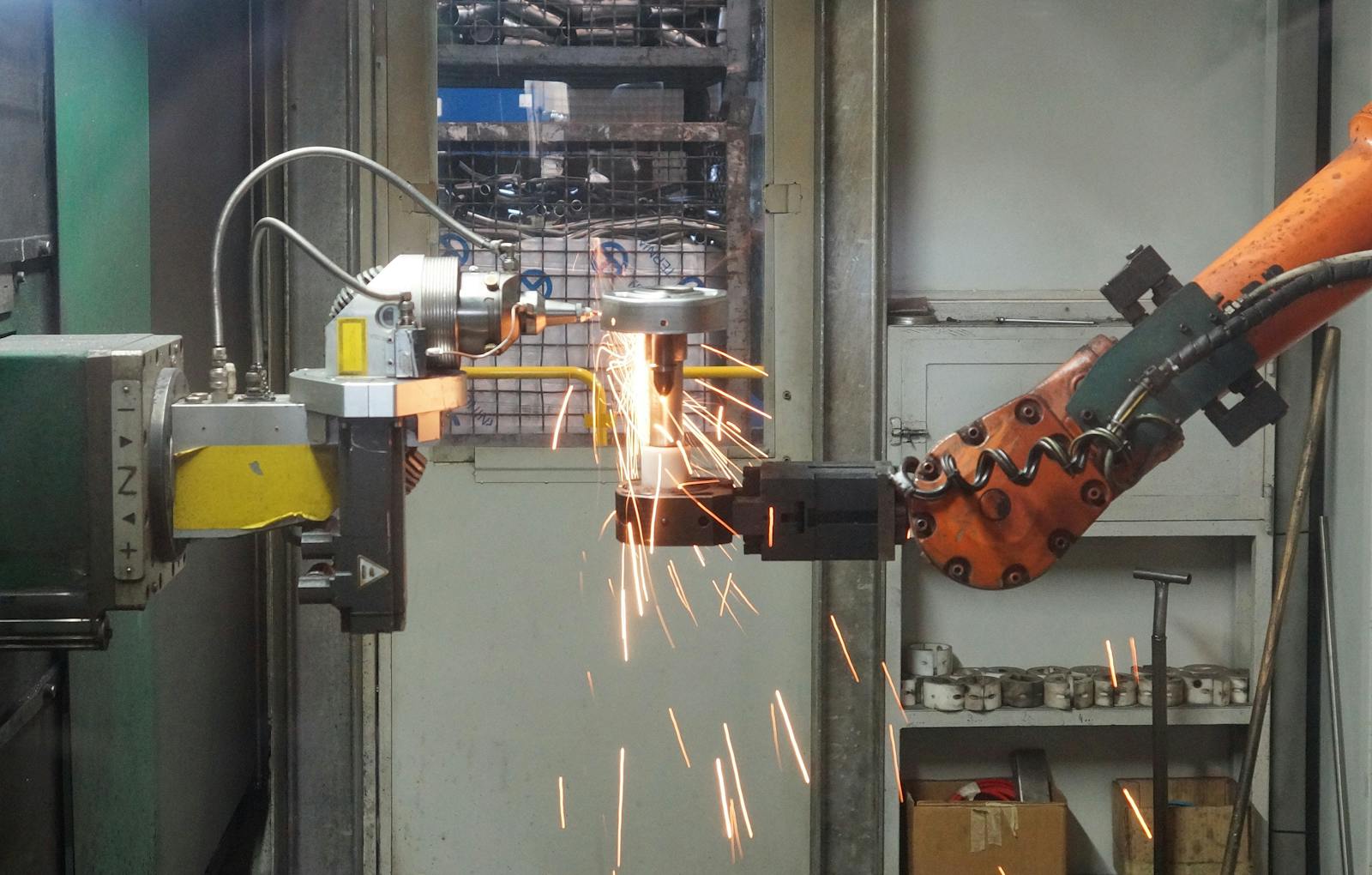

What distinguishes this boom from previous cycles is the type of robots being ordered. Traditional industrial robots, the massive caged arms that weld car frames and stamp metal parts, still make up the bulk of orders. But the fastest-growing segment is collaborative robots, or “cobots,” designed to work alongside humans in logistics, food processing, healthcare, and small-batch manufacturing.

Cobots represented roughly 12% of total robot installations globally in 2024, up from 3% in 2017. Japanese firms like FANUC, Kawasaki Heavy Industries, and startup newcomer MUJIN are investing heavily in AI-enabled cobots that can adapt to unstructured environments, sort irregular objects, and learn tasks through demonstration rather than explicit programming.

A recent study from Tokyo University’s robotics lab found that AI-integrated cobots reduced training time for new manufacturing tasks by 60% compared to traditional programmable systems. For companies struggling to retain experienced workers long enough to train new ones, this matters enormously.

What this means for the global labor equation

Children who grew up watching their parents work factory floors in Nagoya or Shenzhen or Detroit are entering a workforce where the relationship between human labor and automation has fundamentally shifted. The question is no longer whether robots will replace certain jobs. It’s whether there will be enough humans available to do those jobs in the first place.

The International Labour Organization estimates that 14 of the world’s 20 largest economies will face significant labor shortages in manufacturing and logistics by 2030. For countries like Japan, South Korea, and Germany, robotics adoption is less a strategic choice than a survival mechanism.

This dynamic also raises uncomfortable questions about who benefits. Automation tends to concentrate gains among capital owners and highly skilled technicians while hollowing out mid-skill employment. A 2024 NBER study found that regions with higher robot density saw faster GDP growth but also wider income inequality, unless paired with robust retraining programs.

The road ahead

Japan’s government has signaled it intends to maintain the country’s robotics leadership. In April 2025, the Ministry of Economy, Trade and Industry announced a ¥150 billion ($1 billion) subsidy package aimed at next-generation robotics R&D, with particular focus on eldercare robots, agricultural automation, and construction drones. Prime Minister Shigeru Ishiba has framed the investment as central to Japan’s economic security.

Major players are already positioning for the next frontier. FANUC opened a new production facility in Ibaraki Prefecture in March, doubling its monthly cobot output capacity to 11,000 units. Yaskawa Electric announced a joint venture with a South Korean semiconductor firm to develop cleanroom robotics for chip manufacturing, an area of growing geopolitical importance.

For Japan’s robotics industry, the record books tell a story of momentum. But the people running these companies understand that momentum alone doesn’t guarantee permanence. The global labor shortage gives them a tailwind. The question is whether Japanese firms can stay far enough ahead of Chinese competitors, and far enough ahead of demographic reality, to keep their position at the center of how the world builds things.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment